Alzheimer's Care vs General Dementia for Memory Programs

Logan Hassinger

Logan HassingerPublished on: 03/09/2026

Learn the key differences between Alzheimer's care and general dementia memory programs. Discover what type of care your loved one needs.

Stories & Guidance

Real Stories, practical wisdom and emotional support for families navigating senior transitions

Our articles come from real experiences with families just like yours. Each piece is written to address the questions that keep you awake at night, the conversations you're struggling to have, and the decisions that feel impossible to make alone.

Logan Hassinger

Logan HassingerLearn the key differences between Alzheimer's care and general dementia memory programs. Discover what type of care your loved one needs.

Logan Hassinger

Logan HassingerCompare Comfort Keepers vs Home Instead senior care services for Dallas-Fort Worth families. Learn costs, services, and which provider fits your loved o...

Logan Hassinger

Logan HassingerExplore Atria Senior Living pricing, amenities, and financial assistance options for Dallas-Fort Worth families. Find affordable senior care solutions t...

Logan Hassinger

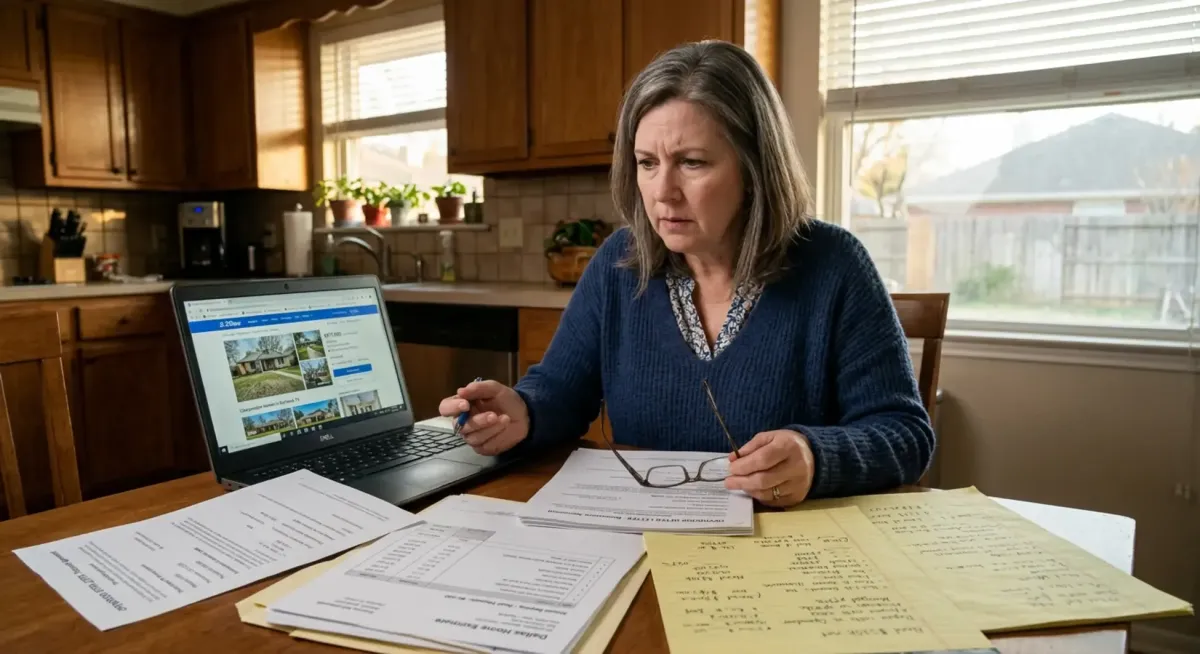

Logan HassingerOpendoor's service fees (5–8%), repair deductions, and hidden costs can significantly reduce what you net from your parent's home sale. Here's what DFW families need to know before accepting any offer.

Logan Hassinger

Logan HassingerWe Buy Ugly Houses vs HomeVestors for your quick sale options, Which is best?

Logan Hassinger

Logan HassingerJubileeTV for dementia caregivers in Dallas-Fort Worth — what it is, what it costs, and whether it's the tool your family has been missing. Includes honest comparison with Zinnia TV and how to fund memory care when the time comes.

Copyright 2026. Sage Senior Support. All Rights Reserved.